Last week, my wife and I welcomed our second child to this world. It was a wonderful experience and no less fascinating than the first time I bore witness to such an event. Aside from all the good feelings and smiles, there are important tax implications of this birth that must be addressed. We will explore the actual and potential impacts on our federal tax liability as a result of the arrival of our little angel.

Dependency Exemption:

Parents of a dependent child like us are entitled to take a dependency exemption on their tax return ($4,050 for 2017). This is a direct reduction to taxable income. Cha-ching! However, this amount is subject to a phase-out for “high income” taxpayers (between $313,800 and $436,300 for Married Filing Joint). To me and my wife, this translates to about $2,025 in tax savings (assuming a 25% bracket).

Child Tax Credit/Additional Child Tax Credit:

Subject to a 7-item test, many taxpayers can get up to $1,000 per child in the form of a tax credit. Unfortunately, this credit is subject to a phase-out as well ($110,000 to $130,000). In addition, the credit is refundable if you have sufficient earned income to cover any excess portion of the credit over your tax liability. Many proud parents will get to knock a few dollars off of their tax bill.

Earned Income Tax Credit (EITC):

Certain “low income” taxpayers that had already been eligible may be able to take better advantage of the EITC by having an additional child. There are different tiers for the credit for those that have from 0 to 3 or more children so your new arrival may put you into the next tier. This will not benefit my family, but can be a significant boon for those that are eligible.

Child and Dependent Care Tax Credit/Flexible Spending Account:

Married taxpayers that both have earned income and have expenses paid to a care provider in excess of those paid by their employer for a dependent child can also receive a nonrefundable credit. There are provisions in the credit that allow for spouse that is a student, seeking employment, and/or disabled to still be eligible to take the credit. The amount of the credit is 20% to 35% of up to $3,000 (or $6,000 if you have 2 or more children) of the expenses paid, phased over $15,000 to $43,000 of income. This sounds complicated, but bear with me – assuming we will hit the $3,000 cap for each child (and we will), this credit will be worth $1,200. It may not sound like much, but I’ll take any help I can get; the cost of daycare is painful. Married taxpayers can also set aside up to $5,000 in pre-tax dollars to a flexible spending account. It is important to note that those funds must be used on qualified expenses in the same year they are set aside or they are lost forever.

Aside from adjusting to sleepless nights and sibling rivalry, we also have to consider the tax ramifications of our fourth family member. There are additional federal and state tax implications to consider, such as saving for college (hoping for scholarships… fingers crossed), student loan interest, and college tuition credits, but the latter two are down the road a ways. For now, we will just have to recognize the advantages that are available to us to help us best plan for the future. Please take this moment to appreciate the simple pleasure of sleeping through the night.

Evan Piccirillo, CPA is a Tax Supervisor in Raich Ende Malter & Co. LLP’s Long Island office. Evan specializes in high net worth individuals, as well as closely-held corporations, S-Corporations, and small businesses. Contact Evan at epiccirillo@rem-co.com or (516) 228-9000.

Evan Piccirillo, CPA is a Tax Supervisor in Raich Ende Malter & Co. LLP’s Long Island office. Evan specializes in high net worth individuals, as well as closely-held corporations, S-Corporations, and small businesses. Contact Evan at epiccirillo@rem-co.com or (516) 228-9000.

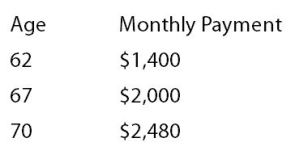

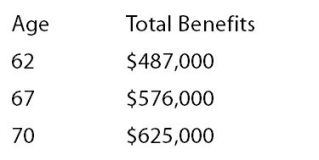

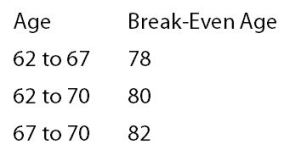

I was talking to a client a few weeks back who said to me, “What do I care? I get a raise at 62 anyway.” He was referring to filing and receiving his social security benefits at age 62 instead of waiting until his full retirement age (FRA). I had to quickly run through a few different scenarios with him and discuss why taking the benefits now instead of waiting may have an adverse effect on his long-term goals. It really resonated with me and made me wonder how many people have the same mindset as that client.

I was talking to a client a few weeks back who said to me, “What do I care? I get a raise at 62 anyway.” He was referring to filing and receiving his social security benefits at age 62 instead of waiting until his full retirement age (FRA). I had to quickly run through a few different scenarios with him and discuss why taking the benefits now instead of waiting may have an adverse effect on his long-term goals. It really resonated with me and made me wonder how many people have the same mindset as that client.

Joseph DeMartinis is a Tax Supervisor in the firm’s Long Island office. He specializes in taxation of small and medium size businesses, their owners, inpatriates, expatriates, and high net worth individuals.

Joseph DeMartinis is a Tax Supervisor in the firm’s Long Island office. He specializes in taxation of small and medium size businesses, their owners, inpatriates, expatriates, and high net worth individuals. Over the last 100 days, we have seen our new President push for many things in any number of directions. The repositioning of certain postures taken during the campaign has ranged from slight to drastic. This in consideration, one word to best sum up the actions of the current administration might be “unpredictable.”

Over the last 100 days, we have seen our new President push for many things in any number of directions. The repositioning of certain postures taken during the campaign has ranged from slight to drastic. This in consideration, one word to best sum up the actions of the current administration might be “unpredictable.”

Evan Piccirillo, CPA is a Tax Supervisor in Raich Ende Malter & Co. LLP’s Long Island office. Evan specializes in high net worth individuals, as well as closely-held corporations, S-Corporations, and small businesses.

Evan Piccirillo, CPA is a Tax Supervisor in Raich Ende Malter & Co. LLP’s Long Island office. Evan specializes in high net worth individuals, as well as closely-held corporations, S-Corporations, and small businesses.

Evan Piccirillo, CPA is a Tax Supervisor in Raich Ende Malter & Co. LLP’s Long Island office. Evan specializes in high net worth individuals, as well as closely-held corporations, S-Corporations, and small businesses.

Evan Piccirillo, CPA is a Tax Supervisor in Raich Ende Malter & Co. LLP’s Long Island office. Evan specializes in high net worth individuals, as well as closely-held corporations, S-Corporations, and small businesses.

Gigi Boudreaux, CPA, MBA is a Tax Partner in Raich Ende Malter & Co. LLP’s Long Island office. She primarily serves small business clients working in the real estate, distribution, manufacturing, and construction industries. She can be reached at

Gigi Boudreaux, CPA, MBA is a Tax Partner in Raich Ende Malter & Co. LLP’s Long Island office. She primarily serves small business clients working in the real estate, distribution, manufacturing, and construction industries. She can be reached at  hange has significant impacts on any foreign person or entity with holdings in U.S. SMLLCs that are disregarded for federal income tax purposes. Previously, these entities were exempt from the comprehensive record maintenance and associated compliance requirements that applied to 25% foreign-owned domestic corporations. Now, substantially any transaction between U.S. domestic disregarded entities and their foreign owners, including any of the owner’s related entities, may be reportable.

hange has significant impacts on any foreign person or entity with holdings in U.S. SMLLCs that are disregarded for federal income tax purposes. Previously, these entities were exempt from the comprehensive record maintenance and associated compliance requirements that applied to 25% foreign-owned domestic corporations. Now, substantially any transaction between U.S. domestic disregarded entities and their foreign owners, including any of the owner’s related entities, may be reportable.

Although the attention has been on who will build the border between the U.S. and Mexico this past year, an even hotter topic in the coming months may be the potential border, both figurative and literal, between the Republican-led House of Representatives and Trump.

Although the attention has been on who will build the border between the U.S. and Mexico this past year, an even hotter topic in the coming months may be the potential border, both figurative and literal, between the Republican-led House of Representatives and Trump.

David Roer is a Tax Manager in Raich Ende Malter & Co. LLP’s New York City office. David specializes in high net worth individuals, as well as closely-held corporations, S-Corporations, and small businesses.

David Roer is a Tax Manager in Raich Ende Malter & Co. LLP’s New York City office. David specializes in high net worth individuals, as well as closely-held corporations, S-Corporations, and small businesses. New York State is so demanding already in terms of personal information required to file your individual tax return. They want your name, address, social security number, date of birth, your income, employer’s name and address… the list goes on and on. Starting in 2016, we get to add another piece of sensitive data to that list: your driver’s license information.

New York State is so demanding already in terms of personal information required to file your individual tax return. They want your name, address, social security number, date of birth, your income, employer’s name and address… the list goes on and on. Starting in 2016, we get to add another piece of sensitive data to that list: your driver’s license information. Evan Piccirillo is a Tax Supervisor in Raich Ende Malter & Co. LLP’s Long Island office. Evan specializes in high net worth individuals, as well as closely-held corporations, S-Corporations, and small businesses.

Evan Piccirillo is a Tax Supervisor in Raich Ende Malter & Co. LLP’s Long Island office. Evan specializes in high net worth individuals, as well as closely-held corporations, S-Corporations, and small businesses. With inauguration day finally behind us, all of the political talk that’s taken over 2016 and 2017 can finally come to an end, right? Wrong. Sad.

With inauguration day finally behind us, all of the political talk that’s taken over 2016 and 2017 can finally come to an end, right? Wrong. Sad. As a general rule, the US has a worldwide taxation system. Effectively, this means that if you’re a US citizen, you pay tax on your worldwide income. This concept is similar for corporations: multi-national corporations (think Apple, Microsoft, or GE) must first pay tax to the foreign country in which the foreign subsidiary does business and earns the profit and then to the IRS, once those profits have been properly repatriated back to the US.

As a general rule, the US has a worldwide taxation system. Effectively, this means that if you’re a US citizen, you pay tax on your worldwide income. This concept is similar for corporations: multi-national corporations (think Apple, Microsoft, or GE) must first pay tax to the foreign country in which the foreign subsidiary does business and earns the profit and then to the IRS, once those profits have been properly repatriated back to the US. David Roer is a Tax Manager in Raich Ende Malter & Co. LLP’s New York City office. David specializes in high net worth individuals, as well as closely-held corporations, S-Corporations, and small businesses.

David Roer is a Tax Manager in Raich Ende Malter & Co. LLP’s New York City office. David specializes in high net worth individuals, as well as closely-held corporations, S-Corporations, and small businesses. Guest Post by Gigi Boudreaux, CPA, MBA

Guest Post by Gigi Boudreaux, CPA, MBA Gigi Boudreaux, CPA, MBA is a Tax Partner in Raich Ende Malter & Co. LLP’s Long Island office. She primarily serves small business clients working in the real estate, distribution, manufacturing, and construction industries. She can be reached at

Gigi Boudreaux, CPA, MBA is a Tax Partner in Raich Ende Malter & Co. LLP’s Long Island office. She primarily serves small business clients working in the real estate, distribution, manufacturing, and construction industries. She can be reached at

{kind=link}